Debt Snowball vs. Debt Avalanche: Which Strategy Is Right for You?

If you’ve ever looked at your debt and thought, “I know I need a plan, but I don’t even know where to start,” you’re not alone.

Debt can feel heavy — not just financially, but emotionally. And often, the stress doesn’t come from the numbers themselves, but from the uncertainty of what to do next.

The good news? You don’t need a perfect plan. You just need a clear one.

Two of the most common and effective debt payoff strategies are the Debt Snowball and the Debt Avalanche. Both work. The key is choosing the approach that feels manageable and keeps you moving forward.

A Quick Check-In

One of the most common questions I hear from clients is:

“Which debt should I pay off first?”

There isn’t a one-size-fits-all answer. But there is a starting point that makes sense for most people.

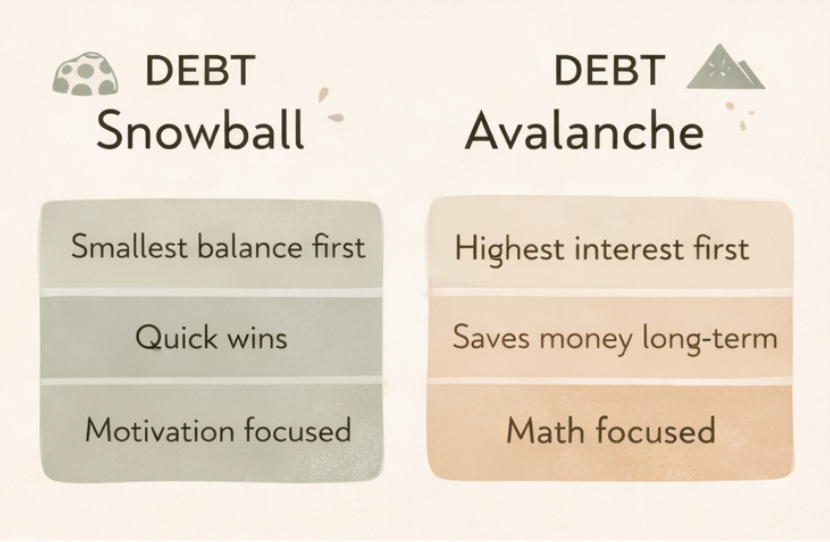

The Debt Snowball Method

The Debt Snowball focuses on building momentum.

You list your debts from smallest balance to largest, pay the minimum on everything, and put any extra money toward the smallest balance first. Once that debt is paid off, you roll that payment into the next one.

Real-Life Example

$500 medical bill

$2,000 credit card

$7,500 car loan

You eliminate the $500 first. That quick win builds confidence and motivation.

Why It Works

Research in behavioral finance shows that people are more likely to stick with a debt payoff plan when they experience early progress. In fact, studies from Harvard Business School have found that focusing on smaller balances first increases the likelihood of completing a debt repayment plan.

This is why I often recommend the Snowball method to my clients. Momentum matters more than math for most people.

That said, I always meet clients where they are. If there’s a high-interest debt or an extenuating circumstance that makes sense to prioritize first, we adjust strategically.

The Debt Avalanche Method

The Debt Avalanche focuses on minimizing interest over time.

You list your debts from highest interest rate to lowest and put extra money toward the highest-interest debt first.

Real-Life Example

Credit card at 24% interest

Personal loan at 11%

Student loan at 5%

You would prioritize the credit card first because it is costing you the most in interest.

Why It Works

Mathematically, this method saves the most money over time. If you are disciplined and motivated by numbers, this can be incredibly effective.

Some studies show that the Avalanche method reduces total interest paid and shortens payoff timelines when someone is highly consistent.

The key word is consistent.

General Tips for Debt Elimination

No matter which method you choose, there are a few principles that must be in place for success:

1. Stop Adding to the Debt

For any method to work, we have to pause the cycle.

It’s okay to temporarily stop using credit cards and rely on your debit card instead. Progress cannot happen if balances keep growing.

2. Adjust Spending Strategically

Sometimes we temporarily adjust saving, investing, or discretionary spending so we can accelerate debt payoff. The goal is not restriction forever — it’s speed and freedom.

Once debt is eliminated, those dollars can go back into your savings and spending buckets with much more momentum.

3. Remember: It’s a Marathon, Not a Sprint

It takes intentional planning each month to get out of debt.

It is often easier to walk into debt than it is to walk out. But with strategy and consistency, it absolutely can be done.

So… Which Method Should You Choose?

The best method is the one you will follow month after month.

For most people, the Snowball method provides the motivation needed to stay the course. But your situation matters.

If you want clarity on which approach makes the most sense for you, I would love to walk through it together.

👉 Schedule a Debt Consultation Here

A Gentle Reminder

Getting out of debt isn’t about perfection. It’s about consistent, strategic progress. Every payment you make is movement forward. And you don’t have to figure it out alone.